In the post-financial crisis era, the most powerful US M&A advisors can be divided into two groups. At the top, the traditionally dominant investment banks, Goldman Sachs and Morgan Stanley. Below them, a coterie of much smaller, boutique firms who have exploited the turmoil at the large universal banks to poach talent and who are winning an increasingly large share of deals.

An FT analysis of deal fees paid between 2014 and 2016 confirms that broad picture, but it exposes some stark realities that are not picked up in the traditional M&A league tables, which typically rank advisers based on the size of the deal, rather than the metric that really matters: fees.

View Wall Street M&A fee rankings

The first is that Goldman is even more dominant than usually recognised. Over the three years to 2016, it earned nearly $2bn as an adviser on the sellside of deals involving US public companies valued at greater than $500m, implying a fee share of greater than 20 per cent. Morgan Stanley, Goldman’s longstanding arch-rival, placed a distant second with a little under $1.3bn in fees. JPMorgan, the bulge bracket bank most unscathed by the financial crisis, finished third with less than half Goldman’s fee income.

Graphics and web development by Claire Manibog.

Where Wall Street's biggest rainmakers are

Sellside M&A fees, US public company targets, 2014-16

Goldman Sachs

Gross deal value ($bn)

700

Morgan Stanley

600

500

Citigroup

400

Centerview

BAML

300

Number of deals

Evercore

200

100

Barclays

JP Morgan

10

100

Qatalyst

Total fees ($m)

0

0

500

1,000

1,500

2,000

Sources: FT research, Dealogic, SEC filings

Where the rainmakers are

Sellside M&A fees, US public company

targets, 2014-16

Gross deal value ($bn)

Goldman Sachs

700

Morgan Stanley

600

500

Citigroup

400

Centerview

BAML

300

Evercore

JP Morgan

200

Barclays

Number of deals

100

100

10

Qatalyst

Total fees ($m)

0

0

500

1,000

1,500

2,000

Sources: FT research, Dealogic, SEC filings

A second, stark reality is that, for all the talk that America’s other universal banks may be about to stage a comeback, Citigroup and BAML remain leagues behind. The international bulge bracket banks Credit Suisse, UBS, and Deutsche Bank do not even rank in the top 10 in the FT analysis and, with lingering difficulties in their home markets, their American renaissance may be some way off.

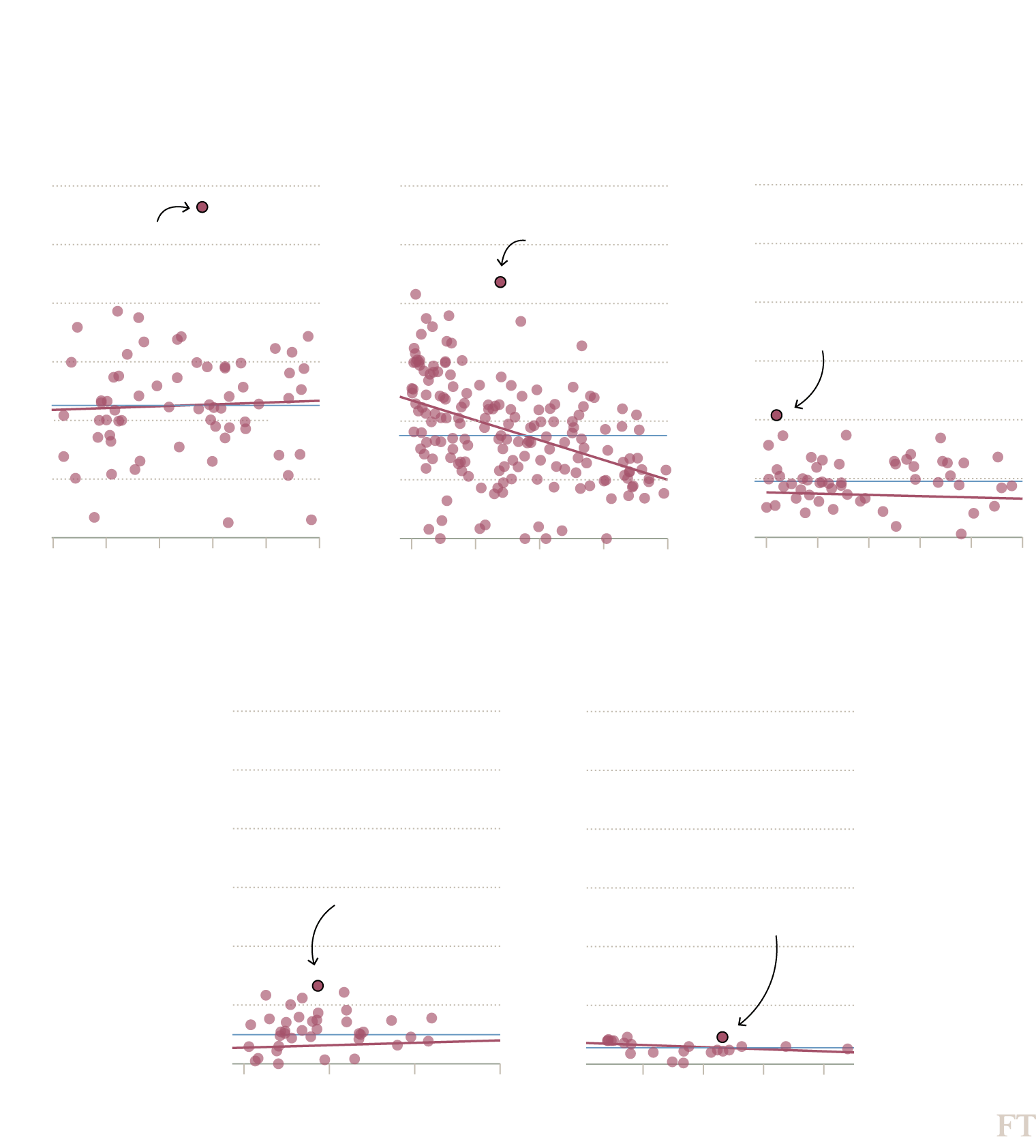

Typically, sellside deal fees are set as a percentage of the company’s equity or enterprise value. The fee rate typically decreases as transaction sizes grow. For example, the average total fee in the FT study for transactions valued at between $1bn and $5bn was 0.92 per cent; for transactions between $10bn and $25bn, the average rate was 0.29 per cent.

Several banks confirmed to the FT that clients that are selling themselves remain highly conscious of fee levels even though, in sale transactions, acquirers ultimately are responsible for paying the fee.

The FT rankings, based on sellside fees disclosed in regulatory documents and collated by Dealogic, show how the universal banks have typically not been able to achieve fees commensurate with those charged by either of their large rivals Goldman and Morgan Stanley or the boutique firms, like Qatalyst, that have sector specialities.

The ability of the boutiques to out-earn much larger rivals is another stark feature of the fee-based rankings, reflecting how they have been able to convince corporate America that they can excel on the biggest deals.

The bulge-bracket banks are, however, gunning to win more business at lower fee rates. "They are interested in high return-on-equity businesses such as M&A,” says Steven Chubak, a research analyst at Nomura Instinet, “so they have become more competitive on compensation and retention of top bankers. This is reflected in our market share data which shows that the big banks have started to improve their position of late.”

The bankers’ rate card

M&A deals by fee (%) and size ($bn)

$500m−$1bn deals

$1bn−$5bn deals

$5bn−$10bn deals

Rate

3.0

3.0

3.0

Target: Trulia

Total fee: $52.1m

Advisors: JPMorgan ($26m), Qatalyst ($26m)

Target: Foundation Medicine

Total fee: $22m

Advisor: Goldman Sachs

2.5

2.5

2.5

Target: NPS Pharmaceuticals

Total fee: $54m

Advisors:

Goldman Sachs ($36m),

Leerink Partners ($18m)

2.0

2.0

2.0

1.5

1.5

1.5

Median

1.0

1.0

1.0

Median

Median

0.5

0.5

0.5

0.0

0.0

0.0

5

6

7

8

9

10

0.5

0.6

0.7

0.8

0.9

1.0

1

2

3

4

5

Deal size

$10bn−$25bn deals

$25bn and greater

3.0

3.0

2.5

2.5

2.0

2.0

Target: Monsanto

Total fee: $155m

Advisors:

Morgan Stanley ($120m),

Ducera Partners ($35m)

Target: Medivation

Total fee: $95m

Advisors:

JPMorgan ($51.3m),

Evercore ($43.7m)

1.5

1.5

1.0

1.0

0.5

0.5

Median

Median

0.0

0.0

10

15

20

25

40

60

80

100

Source: FT research, Dealogic, SEC filings

The bankers’ rate card

M&A deals by fee (%) and size ($bn)

$500m−$1bn deals

$1bn−$5bn deals

$5bn−$10bn deals

Rate

Target: Trulia

Total fee: $52.1m

Advisors:

JPMorgan ($26m),

Qatalyst ($26m)

3.0

3.0

3.0

Target: NPS Pharmaceuticals

Total fee: $54m

Advisors:

Goldman Sachs ($36m),

Leerink Partners ($18m)

Target: Foundation Medicine

Total fee: $22m

Advisor: Goldman Sachs

2.5

2.5

2.5

2.0

2.0

2.0

1.5

1.5

1.5

Median

1.0

1.0

1.0

Median

Median

0.5

0.5

0.5

0.0

0.0

0.0

5

6

7

8

9

10

0.5

0.6

0.7

0.8

0.9

1.0

1

2

3

4

5

Deal size

$10bn−$25bn deals

$25bn and greater

3.0

3.0

Target: Monsanto

Total fee: $155m

Advisors:

Morgan Stanley ($120m),

Ducera Partners ($35m)

2.5

2.5

Target: Medivation

Total fee: $95m

Advisors:

JPMorgan ($51.3m),

Evercore ($43.7m)

2.0

2.0

1.5

1.5

1.0

1.0

0.5

0.5

Median

Median

0.0

0.0

10

15

20

25

40

60

80

100

Source: FT research, Dealogic, SEC filings

The bankers’ rate card

M&A deals by fee (%) and size ($bn)

$0.5bn−$1bn deals

Rate

3.0

Target: Foundation Medicine

Total fee: $22m

Advisor: Goldman Sachs

2.5

2.0

1.5

Median

1.0

0.5

0.0

0.5

0.6

0.7

0.8

0.9

1.0

Deal size

$1bn−$5bn deals

3.0

Target: Trulia

Total fee: $52.1m

Advisors: JPMorgan ($26m), Qatalyst ($26m)

2.5

2.0

1.5

1.0

Median

0.5

0.0

1

2

3

4

5

$5bn−$10bn deals

3.0

2.5

Target: NPS Pharmaceuticals

Total fee: $54m

Advisors:

Goldman Sachs ($36m),

Leerink Partners ($18m)

2.0

1.5

1.0

Median

0.5

0.0

5

6

7

8

9

10

$10bn−$25bn deals

3.0

2.5

2.0

Target: Medivation

Total fee: $95m

Advisors:

JPMorgan ($51.3m),

Evercore ($43.7m)

1.5

1.0

0.5

Median

0.0

10

15

20

25

$25bn and greater

3.0

2.5

2.0

Target: Monsanto

Total fee: $155m

Advisors:

Morgan Stanley ($120m),

Ducera Partners ($35m)

1.5

1.0

0.5

Median

0.0

40

60

80

100

Source: FT research, Dealogic, SEC filings

One longtime adviser at a top boutique said of Citigroup and BAML: “They are coming back. They now have better balance sheets and better health. Our position does not feel as firm.” However, another cautioned that no universal bank had built an M&A franchise that was strong across all sectors of corporate America. “The mid-tier firms have an industry group or two that is strong. But Goldman and Morgan Stanley are either number one or number two in every sector.”

For Goldman Sachs, the pressure to remain at the top of the heap is perhaps stronger now than at any time in recent years. M&A revenues have become a more significant part of its revenues and its ability to meet company-wide return on equity targets. In 2007, before the financial crisis, overall investment banking revenue was 16 per cent of the group total. That proportion had risen to 21 per cent in 2016.

One Goldman banker noted the pressure and said the bank was considering smaller deals today than it would have previously, just to continue to generate fees.

Goldman attributes its dominant sellside franchise to two factors: its deep relationships with clients and its overall experience and longevity. “When you are on the sellside, you really have to know your clients’ business”, said Michael Carr, co-head of global M&A at the bank.

He added: “If there is a problem that is really vexing, I can walk down the hall and there is 100 years of experience 50 yards away. We pride ourselves on being able to answer any question that could come up in a boardroom.”

Goldman’s vast network, however, has got it into trouble in the past. It represented energy pipeline company El Paso in its $21bn sale to rival Kinder Morgan in 2011. At the same time, a Goldman banker representing El Paso owned Kinder Morgan stock while the bank’s private equity division also owned a fifth of Kinder Morgan. After a shareholder lawsuit alleging conflicts of interest, Goldman agreed to forfeit its $20m M&A fee as part of a settlement.

Issues such as these have been exploited by the boutique firms who market themselves as having none of the large bank’s potential for conflicts and less likely to have transaction details leak. They are also seized upon by rivals at other banks.

Still, one executive whose company used both Goldman and a large universal bank to handle its sale experienced the Goldman modus operandi at close quarters.

“The banker at the large firm had done a ton of free work for us for years so we threw him a few million dollars as bone. But he could not have gotten us the 40 per cent above our all-time high that we got,” he said. “Goldman had the poker tactics, down to telling our management not to even talk to the buyers in the bathroom during due diligence. We went to them when we needed the A team. Other bankers didn’t have their nuts of steel.”

Sign up to receive Due Diligence, our essential newsletter to help you find your way through the complex world of mergers and acquisitions.

Wall Street M&A fee rankings

| Average fees on deals of: | |||||||||||

| Ranking | Firm | Market share (%) | Total revenue ($m) | Total deal value ($m) | Deals | Avg deal size ($m) | $5m-$1bn | $1bn-$5bn | $5bn-$10bn | $10bn-$25bn | $25bn and over |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Goldman Sachs | 21.8 | 1,957 | 662,867 | 73 | 9,080 | 1.29 | 0.81 | 0.45 | 0.26 | 0.90 |

| 2 | Morgan Stanley | 14.1 | 1,270 | 580,579 | 48 | 12,095 | 1.36 | 0.95 | 0.42 | 0.22 | 0.10 |

| 3 | JP Morgan | 10.4 | 940 | 243,355 | 40 | 6,084 | 1.80 | 0.90 | 0.36 | 0.22 | |

| 4 | Centerview | 8.4 | 752 | 315,035 | 24 | 13,126 | 1.10 | 0.53 | 0.24 | 0.90 | |

| 5 | BAML | 6.7 | 606 | 281,191 | 31 | 9,071 | 1.20 | 0.78 | 0.26 | 0.21 | |

| 6 | Qatalyst | 6.3 | 567 | 88,125 | 17 | 5,184 | 1.26 | ||||

| 7 | Citigroup | 5.4 | 482 | 398,048 | 23 | 17,306 | 0.42 | 0.33 | 0.70 | ||

| 8 | Barclays | 3.3 | 300 | 145,348 | 20 | 7,267 | 1.48 | 0.78 | |||

| 9 | Evercore | 3.0 | 271 | 233,486 | 18 | 12,971 | 0.32 | 0.35 | 0.30 | ||

| 10 | Lazard | 2.7 | 240 | 141,927 | 13 | 10,917 | 0.74 | 0.27 | 0.14 | ||

| 11 | Guggenheim | 2.6 | 235 | 105,708 | 8 | 13,214 | 0.81 | ||||

| 12 | Credit Suisse | 2.3 | 210 | 96,733 | 13 | 7,441 | 0.73 | 0.19 | |||

| 13 | Allen | 1.6 | 145 | 201,592 | 5 | 40,318 | |||||

| 14 | Deutsche Bank | 1.2 | 104 | 14,805 | 8 | 1,851 | 0.65 | ||||

| 15 | Jefferies | 1.0 | 89 | 80,081 | 11 | 7,280 | 1.11 | 0.26 | |||

| 16 | Sandler O'Neill | 1.0 | 87 | 15,633 | 8 | 1,954 | 0.92 | 0.65 | |||

| 17 | Wells Fargo | 0.7 | 65 | 15,800 | 5 | 3,160 | 0.61 | ||||

| 18 | Perella Weinberg | 0.7 | 63 | 15,391 | 4 | 3,848 | |||||

| 19 | UBS | 0.6 | 57 | 36,834 | 6 | 6,139 | |||||

| 20 | Moelis | 0.5 | 45 | 20,473 | 5 | 4,095 | |||||

| 21 | Greenhill | 0.5 | 43 | 28,606 | 7 | 4,087 | 0.57 | ||||

| 22 | BMO | 0.4 | 40 | 45,268 | 2 | 22,634 | |||||

| 23 | MTS | 0.4 | 35 | 2,928 | 3 | 976 | |||||

| 24 | Ducera | 0.4 | 35 | 66,341 | 1 | 66,341 | |||||

| 25 | LionTree | 0.4 | 35 | 6,071 | 2 | 3,036 | |||||

| 26 | KBW | 0.4 | 33 | 5,008 | 3 | 1,669 | |||||

| 27 | RBC | 0.3 | 28 | 8,234 | 3 | 2,745 | |||||

| 28 | Zaoui | 0.2 | 22 | 7,737 | 1 | 7,737 | |||||

| 29 | Stifel | 0.2 | 21 | 4,072 | 3 | 1,357 | |||||

| 30 | Piper | 0.2 | 21 | 2,320 | 2 | 1,160 | |||||

| 31 | Macquarie | 0.2 | 20 | 5,784 | 2 | 2,892 | |||||

| 32 | Tudor | 0.2 | 19 | 21,302 | 4 | 5,326 | 0.13 | ||||

Methodology: Fee data reflect acquisitions of US public companies, in deals valued at more than $500m announced between January 1, 2014 and December 31, 2016 that have closed or remain pending. Deal value is the greater of transaction enterprise value or equity value, as per Dealogic definition. Data compiled by Dealogic from fees disclosed in Securities and Exchange Commission filings. Note: US public sellside fees reflect only a fraction of overall firm advisory revenues.